Blog

BLOG

Blog

We recently attended the 2025 Capstone Title Economic and Real Estate Forecast and are excited to share noteworthy insights on the economy, markets, real estate and more.

This guide dives into frequently asked questions regarding the 1031 Exchange process and provides comprehensive answers that will leave you feeling more confident about your Exchange.

Why Choose a 1031 Improvement Exchange? A 1031 Improvement Exchange can be a great way for property investors to turn what would otherwise be a partial exchange “with Boot” into a full Exchange which defers capital gains tax. Boot refers to the excess cash created when a Replacement Property is purchased for a lower price than the Relinquished Property is sold for, and this difference is taxable. However, if the Replacement Property is a candidate for Improvements that can be completed within the 180-day 1031 Exchange timeline requirement, a 1031 Improvement Exchange can be used. To take full advantage of a 1031 Improvement Exchange, investors often focus on efficiently using up the excess cash for improvements that will add the most value to the property, such as clearing land, enhancing driveways, adding or repairing fencing, replacing roofs or remodeling the interior. Note, when determining where to focus, investors need to consider that improvements which require complex planning or permitting can be difficult to accomplish in a limited time frame.

Why Choose a 1031 Reverse Exchange? A 1031 Reverse Exchange allows investors to capitalize on lucrative investment opportunities without being constrained by the immediate sale of their existing property, which results in greater flexibility and control over their investment decisions. The 1031 Reverse Exchange is more commonly used when an Exchanger: Finds the exact Replacement Property they want to purchase and doesn’t want to risk losing it Needs time to transition a business to a new location while minimizing or eliminating downtime

Explore the power of 1031 exchanges in investment strategies. Learn how savvy investors strategically unlock wealth multiplication through real estate transactions.

Discover the financial advantage of a 1031 exchange and enhance your wealth-building potential.

This blog guides you through the intricate 1031 exchange timelines with a focus on the year-end.

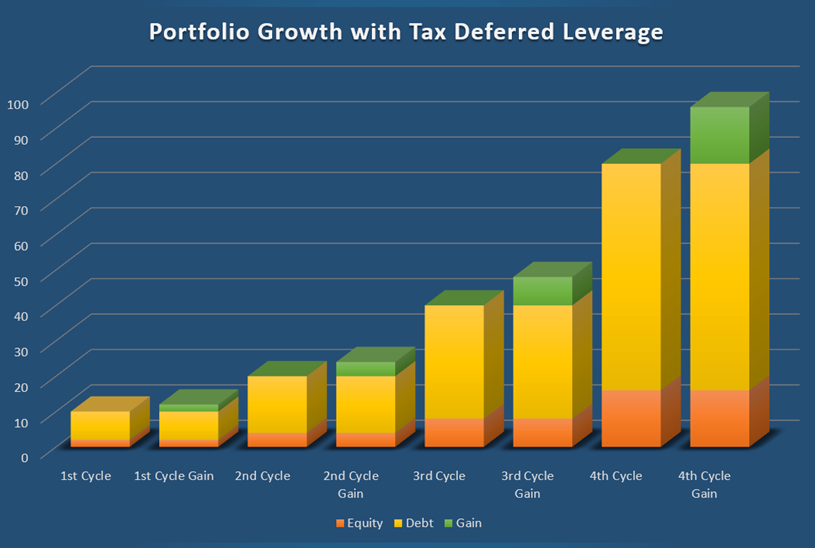

Investing in real estate is not just about owning properties; it's about growing wealth over time. One of the most effective tools for maximizing the potential of your real estate investments is the 1031 Exchange. In this section, we'll explore how a well-executed 1031 Exchange can lead to the realization of wealth multiplication and substantial portfolio growth. The accumulation of equity gains in a property over time creates a remarkable snowball effect. As you make mortgage payments and the property appreciates, your equity stake increases. The longer you hold a property, the faster this effect grows. For instance, if you initially invest with a 20% equity stake, this percentage can increase as your property appreciates and mortgage balance reduces. As a result, your wealth potential multiplies. Portfolio Growth A well-executed 1031 Exchange can be a game-changer for your real estate portfolio. By capturing equity gains and transitioning into new properties while deferring these tax liabilities, investors can witness significant portfolio growth. The key to this strategy is repetition. With each 1031 Exchange cycle, you continue to leverage your equity gains, allowing your portfolio to expand exponentially, all while enjoying the benefits of tax deferment. This approach enables you to make the most of your assets' appreciation, maintain steady growth, and ensure that your wealth multiplication is optimized.

Most investors have heard that the IRS requires a 1031 Exchange to be completed within a maximum time period of 180 days from start to finish, but what many don’t realize is that IRS Section 1031 actually imposes two possible deadlines, and it applies whichever one occurs first. The most well-known deadline is, or course, the 180-day maximum, but the second one that could cut that period short is the Due Date for the Taxpayer's Tax Return. Say you sell your relinquished property late in the year, sometime after October 18 th , which means that your 180-day exchange period would extend beyond April 15 th of the following year. If you are filing an individual or joint tax return, including LLC's reporting on an individual or joint tax return, the Exchange Period would be limited by the earlier April 15 th Tax Due Date. The most extreme example of this would be an exchange that begins with a sale on December 31st, which would leave only 105 days left until April 15 th . Luckily the solution is simple, if you need the extra time to complete the exchange, make sure to file an extension that extends the Due Date for your tax return beyond the end of the 180-day Exchange Period. This will ensure that you get your full 180 days to complete the Exchange. Logically this rule does make sense because filing a 1031 Exchange requires two parts. The first is reporting the sale of the relinquished property asset and the second is reporting what you received in exchange, which would be one or more replacement properties. It would not be possible to report the outcome of the exchange until all purchases were complete, so filing a tax return in the middle of the process would not work. The other outcome of this provision is to ensure that all 1031 Exchanges are reported in the tax filing year in which the Exchange started and are not carried over into the next tax filing year.

Welcome to our new website! This site has been professionally designed to be responsive and mobile friendly, so it looks great and is accessible no matter what type or size of device you are using. Our new website also has an integrated Client Portal, meaning you are able to access your case documents, correspondence, and calendars directly from our website! If you have any questions, don’t hesitate to contact us today.

Address

901 S. Mopac Exp, Bldg II, Ste 150

Austin, TX, 78746

Business Hours

Monday - Friday

9:00 AM - 5:00 PM

Central Time

Ten31 Texas, LLC

This website has been built to be accessible for all users. If you experience any difficulty in accessing this website, please contact us for assistance.